For Keir Starmer’s launch of the Labour Party’s Climate Mission on 19 June in Edinburgh, Transition Economics was asked by Labour to conduct an independent assessment of the potential increased investment and increased jobs in target areas in the UK’s industrial heartlands that could be catalysed by the Labour Party’s proposed British Jobs Bonus.

The briefing estimates that new jobs catalysed by the British Jobs Bonus could be 19,300 in Year 1, rising to 64,600 in Year 5.

In 2030, this breaks down

as 35,200 jobs in English regions

19,300 jobs in Scotland

5,800 jobs in Wales

4,300 jobs in Northern Ireland.

The analysis also finds that the British Jobs Bonus can increase local construction and manufacturing investment from offshore wind, onshore wind, solar and green hydrogen development in target areas by £1.7bn in Year 1 of a Labour government, rising to £5.9 billion in Year 5.

Crown Estate Scotland announced the outcome of the ScotWind Lease round in January 2022, with 17 projects awarded option agreements. The 17 projects have a potential total capacity of almost 25 GW of offshore wind – both floating and fixed.

Transition Economics has analysed the ownership and jobs potential outcomes of ScotWind lease round for the Scottish Trades Union Congress. This analysis was covered by The Herald’s here.

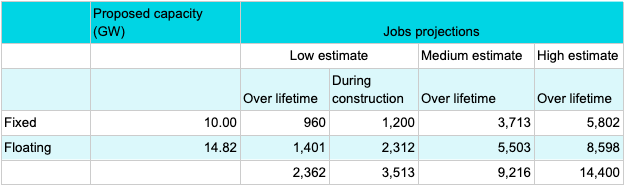

Potential Job Creation from ScotWind leases

Transition Economics has modelled the potential job creation from the 17 proposed offshore wind projects, over the lifetime of the projects during pre-development, construction and the operational phase. In our low estimate, we also broke this down into job creation during the construction phase.

In a scenario with high levels of local content and significant domestic fabrication, 14,400 jobs could be created in Scotland across the lifetime of offshore wind farms.

However, in a scenario with limited local content – primarily focused on pre-development, operations and maintenance and limited installation – the 17 offshore wind farms could deliver less than 2,500 Scottish jobs over the same period.

Our methodologies for estimating job creation from new offshore wind projects was developed in our analysis for the Scottish Trades Union Congress, and published in the Green Jobs in Scotland report in April 2021. Jobs “over lifetime” include pre-development, construction and installation, operations & maintenance, and decommissioning.

Crucially, reaching the medium or high end estimates will require significant pro-active government measures to drive investment and expansion of the Scottish offshore wind supply chain – beyond current government policies.

In response to the ScotWind lease results being announced, the Scottish Government said that“Because Scotland’s workers are superbly placed with transferable skills to capitalise on the transition to new energy sources, we have every reason to be optimistic about the number of jobs that can be created.

That means, for example, that people working right now in the oil and gas sector in the North East of Scotland can be confident of opportunities for their future.”

“The spread of projects across our waters promises economic benefits for communities the length and breadth of the country, ensuring Scotland benefits directly from the revolution in energy generation that is coming.”

To ensure the desired job creation becomes a reality, the Scottish Government should enact appropriate policies, such as:

Public investment of £2.5 billion – £4.5 billion to 2035 in ports and manufacturing to supply large scale offshore renewables

Setting up a Scottish National Energy Company, to participate in developing and deploying new offshore wind farms

Expand local content (as practiced in France, Turkey, Taiwan and elsewhere) and local hiring requirements, with stronger accountability measures to ensure targets are met

Skills programmes to address shortages, and remove barriers to renewables jobs for oil and gas workers.

2. Analysis of Ownership

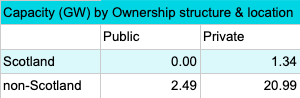

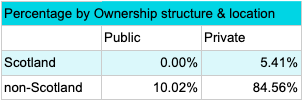

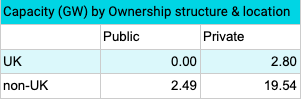

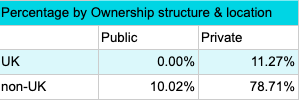

Transition Economics has analysed the ownership structures and countries of origin for the 26 parent companies behind the joint ventures acquiring the 17 ScotWind leases. This enabled us to create a breakdown of the proposed offshore wind capacity (in GW) by location and by public or private ownership structure.

The best majority of the leases are owned by companies ultimately based outside Scotland: over 23GW, representing 95% of the total. Only 1.3GW are owned by companies based in Scotland.

2.5 GW of proposed capacity (10% of the total) are controlled by publicly-owned entities, from Sweden, Denmark, Belgium and Germany. The remainder (90%) is owned by private companies. None of the proposed new wind farms have ownership participation from public UK or Scottish entities.

This analysis, commissioned by Platform London, shows that UK local authority pension funds that are not divesting from fossil fuel companies could have lost at least £1.75 billion in value over the past three years as a result of investments into just nine oil & gas companies.

56 pension funds were identified as holding direct investments into oil companies and not having made public commitments to reduce direct fossil fuel holdings. These funds’ combined direct investments into nine oil companies were valued at £3.6 bn in spring 2017, and would have dropped to £1.8 bn by November 2020.

The three funds losing the most value have all publicly opposed divesting direct holdings.

Greater Manchester Pension Fund was the most exposed, potentially losing £375 million in value, or 2.2% of its total holdings. This is equivalent to £1,000 per pension member.

West Yorkshire Pension Fund was second most exposed in terms of total value, losing £211 million in value. This is equivalent to £740 per pension member.

Nottinghamshire was third with £81 million, equivalent to £1,070 per pension member.

In early 2020, Reuters reported Greater Manchester and West Yorkshire funds as claiming they would have lost £400m and £160m respectively over 3 years to 2019, if they had divested from fossil fuels. The losses by 2020 on only the nine top oil companies almost entirely eradicate this gain. Share values are volatile, and regularly rise and fall. However, repeated Financial Times reporting on the falling asset values and impairments amongst big oil companies describes this not as a temporary downturn, but as “the direction of travel” . Despite the expected continued use of fossil fuels in some industries for many years, the push to net zero will hit the underlying business model of large oil & gas companies significantly – especially those that rely on high oil prices to turn profits.

Analysis and modelling carried out by Transition Economics for the TUC’s Voice and Place report provides a regional analysis of clean infrastructure investment options, and the resulting potential for direct job creation.

This analysis demonstrates the regional distribution (at NUTS1 level) of 506,000 English and Welsh potential direct jobs, including in rail upgrades, EV charging, cycles lanes and pedestrianisation, home energy efficiency retrofits, social housing construction, and reforestation.

It also provides job creation estimates for priority industrial policy proposals for a just climate transition in England and Wales identified in the TUC’s Voice & Place report, including battery gigafactories, manufacturing for offshore wind, steel and district heating.